Factors across macro regimes

Macro

Markets

Exploring factor performance across macro regimes

Excellent piece by SP Global research.

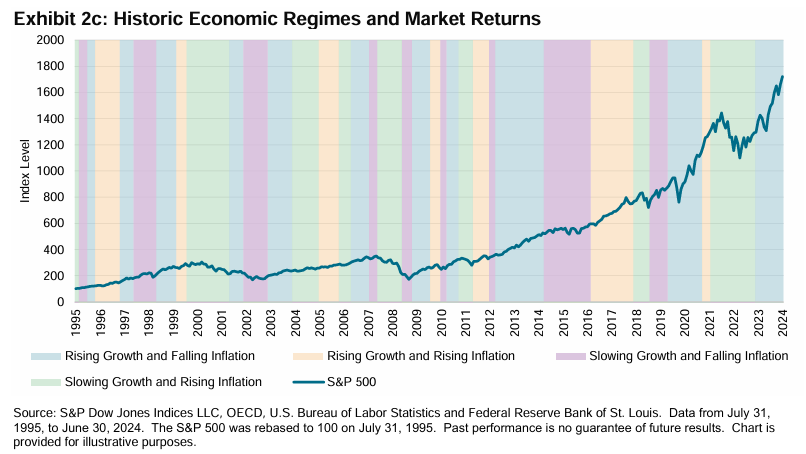

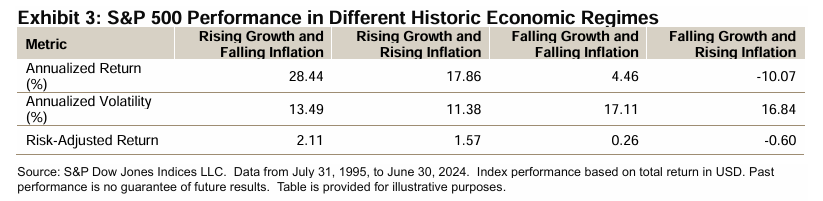

First they define macro regimes in the class 4 quadrant approach.  Then the compute SP500 performance within each regime

Then the compute SP500 performance within each regime

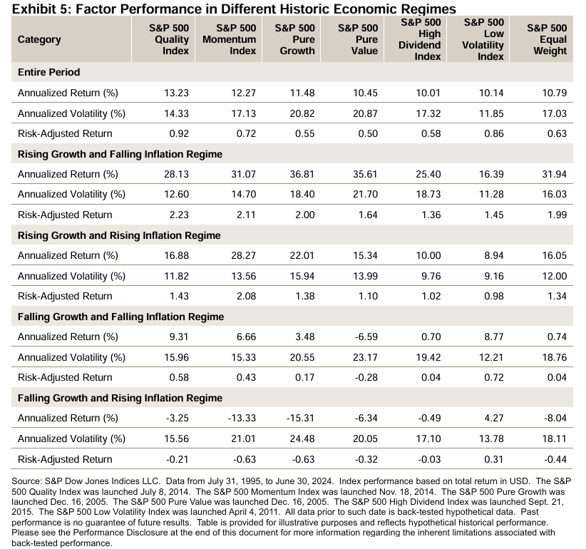

Finally, they compute factor performance within each regime

I would have loved to have seen statistical testing to compare these performance metrics (e.g. Ledoit and Wolfe). Causal inspection suggests there is a material difference, but I’d prefer to have statistical support.